Market intelligence report

Here we look at the market's strong start in 2026 and the potential drivers impacting production and demand over the coming months.

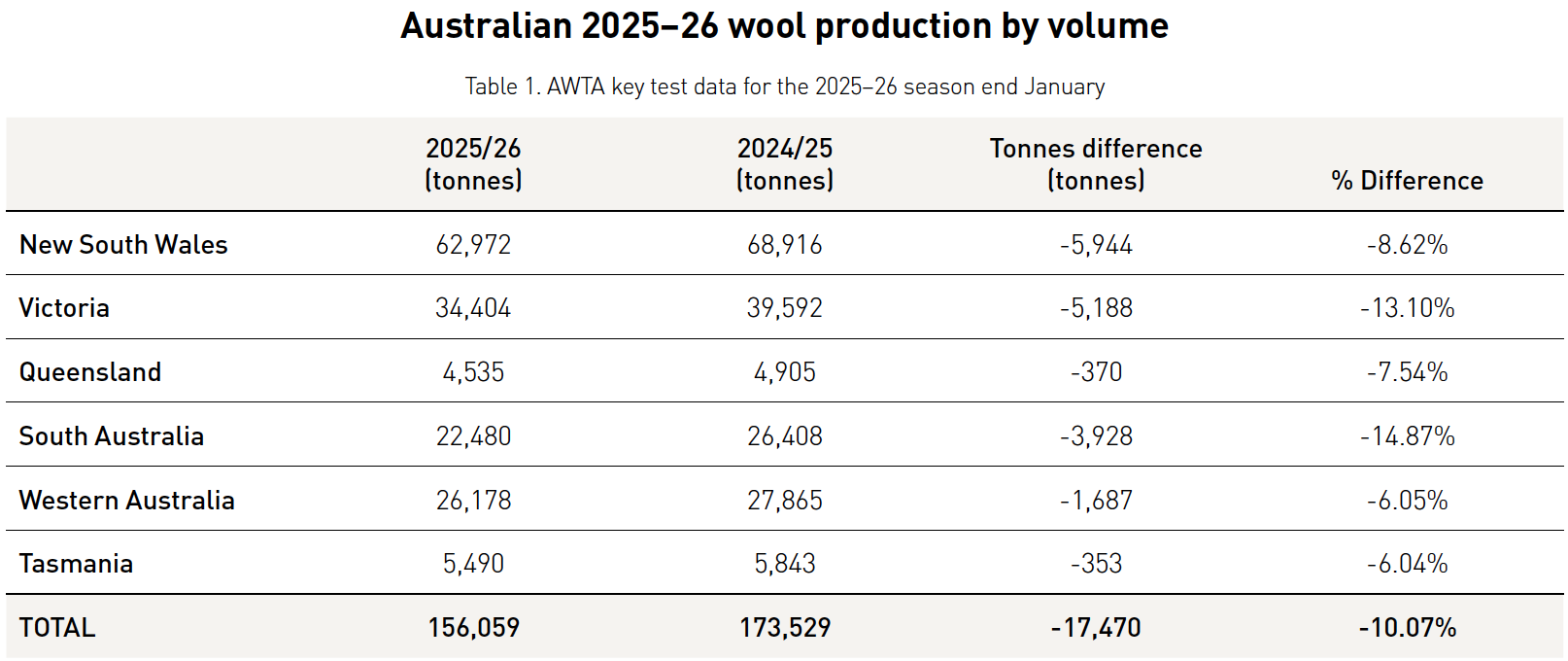

All states have continued to record a downward trend in testing throughput year-to-date (ending January). Year-on-year, the largest declines were seen in South Australia and Victoria seeing 14.87% and 13.10% reductions respectively, largely due to harsh drought conditions with recent bushfire events in Victoria causing more pain for growers. New South Wales is also experiencing drought conditions particularly in Southern New South Wales, seeing a reduction of 8.62%. Seven months into the 2025/26 wool growing season has the total wool tested running 10.07% below the 2024/25 season total.

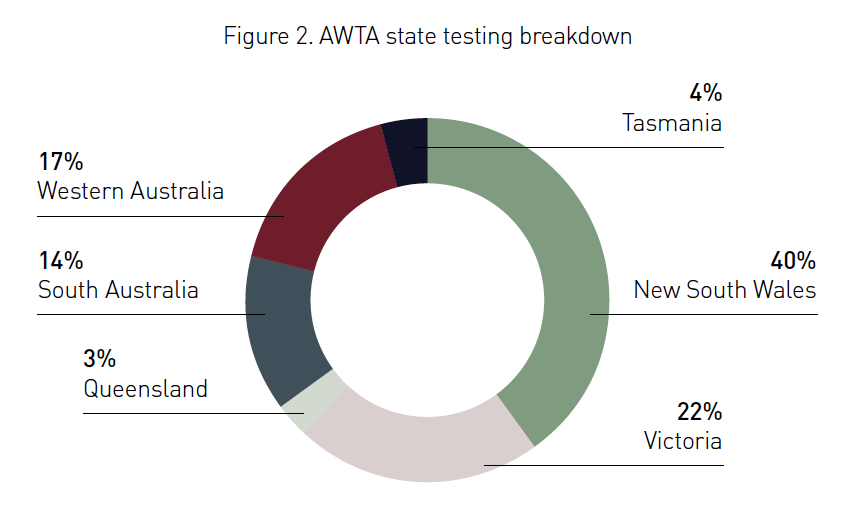

New South Wales continues as the largest wool producing state at 40%, followed by Victoria at 22% accounting for 62% of total Australian wool tested. Comparing this to the 2024/25 season, this is in line with New South Wales and Victoria finishing last season with 62% of all wool tested. Similarly, the other states remain in line with 24/25 season percentage totals.

Wool auction offering update –

AWEX Auction data (as of week 31 sale)

- Offered 914,215 bales compared to the 942,043 bales offered last season. That is 27,828 bales less, or 3% less wool offered.

- Sold 853,273 bales compared to the 870,671 bales sold last season. That is 17,398 bales less, or 2% less wool sold.

- Clearance rates this season are running at 93.3% compared to 92.3% cleared over the same period last season.

- Total value sold through the auction system is A$1,465 million, compared to A$1,186 million last season at the same time. This is an increase of A$279 million, or 19% higher year-on-year.

Offering statistics this season to date point to firmer wool values despite a reduction in overall supply. Looking ahead, supply constraints may become more pronounced, with AWTA testing volumes down around 10% year-on-year, while auction offerings are only 3% lower.

This divergence is most evident in Western Australia, where auction offerings are up 3.5% year-on-year, yet testing volumes remain down 6%. In contrast, southern auction offerings are down 6.6%, while northern offerings are only 0.1% lower, reflecting the seasonal growing conditions.

The data suggests current throughput is being supported by a drawdown of broker-held stocks and previously prepared wool. As this short-term buffer is progressively worked through, tighter supply conditions are likely later in the season if testing volumes remain subdued. This prevailing supply shortage will look to underpin prices moving through the 2026 calendar year.

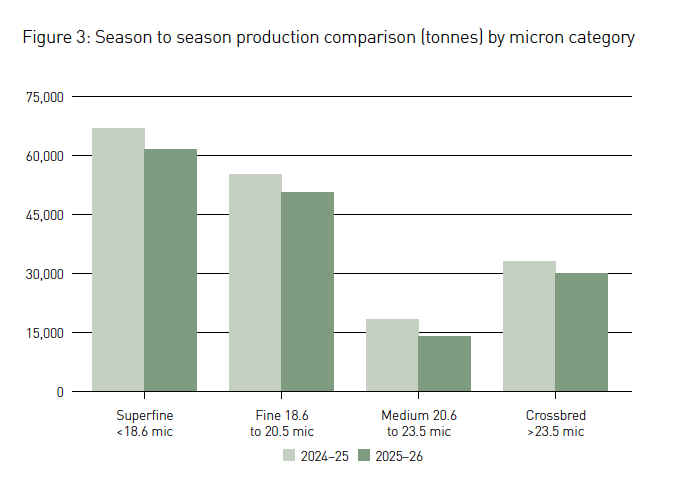

Production by micron – AWTA testing data (January)

The largest year-on-year losses are concentrated through the 17.6–21.6 micron range, which represents the core of the Merino clip. The losses are less pronounced in the superfine Merino types. This likely reflects a shift in the clip toward finer micron under tougher seasonal conditions and/or changes in the mix of wool presented for testing. Despite this, the largest reductions remain concentrated in the core 17.6–21.6 micron range, which continues to drive the overall decline in throughout.

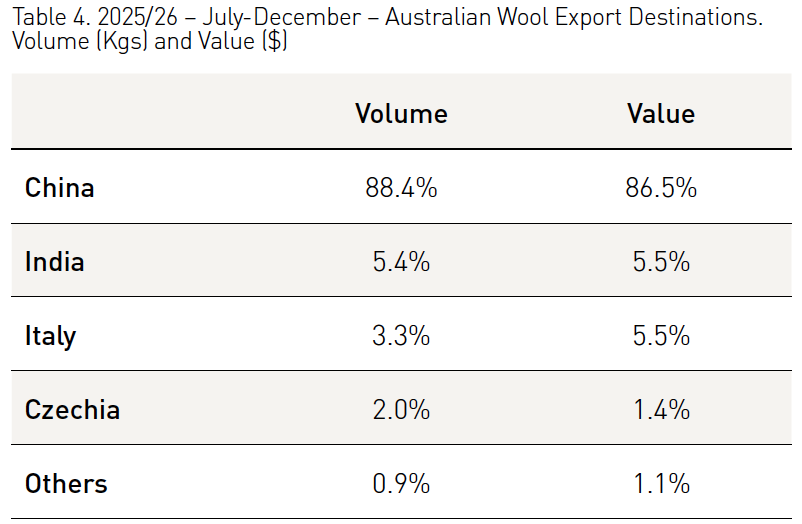

Australian wool exports – ABS data (2025–26 season)

Australian wool exports declined on a year-on-year basis over the July to December period, with shipment volumes down 8.9% in kgs of greasy wool. China remained the dominant destination, accounting for 88.4% of total exports, although volumes shipped declined by 6.3% compared with the same period last year. India continued to rank as the second-largest importer of Australian wool, however volumes were down 3.8% year-on-year.

In contrast, Italy recorded an increase in volumes of 6.3%, while shipments to Czechia fell sharply, declining by 23.2% year-on-year. In value terms, Australian wool exports were 0.2% lower compared with the previous year. Export values to China have increased modestly by 3.2% year-on-year, while still accounting for 86.5% of total export value. Czechia again recorded a significant fall in value, down 19.9%. In contrast, both India and Italy posted year-on-year increases in export value of 15% and 15.9% respectively, indicating relatively firmer price outcomes in these markets despite lower or modest shipment volumes.

It is worth noting that, despite recent improvement, Italian wool imports remain well below historical trend levels in both volume and value. However, the year-on-year increases recorded in both measures point to improving demand conditions, particularly from premium wool apparel markets. This marks the first time in several years that Italy has recorded positive movements in both value and volume, providing early signs of improving offshore demand for Australian wool in this market. While higher wool prices have likely contributed to the lift in export values from relatively low levels, the 6.3% increase in shipment volumes into Italy is a positive development and suggests some gradual improvement in demand.

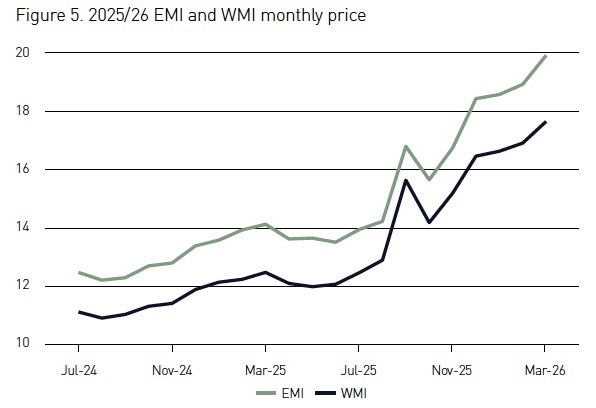

Wool pricing update – To the 36th sale week

Since the start of the current season to the 36th sale week, both the Eastern Market Indicator (EMI) and Western Market Indicator (WMI) have been well supported and have trended higher overall. By 4th March, the EMI had lifted by 45.8%, while the WMI increased by approximately 47.2% over the same period. Although both indices softened during October/November, they stabilised and strengthened into January, finishing close to seasonal highs. The strong lift through February suggests firmer market sentiment and improved buyer confidence, supported by tightening supply conditions through the auction system. However, the pace of recent gains also highlights the potential for increased short-term volatility.

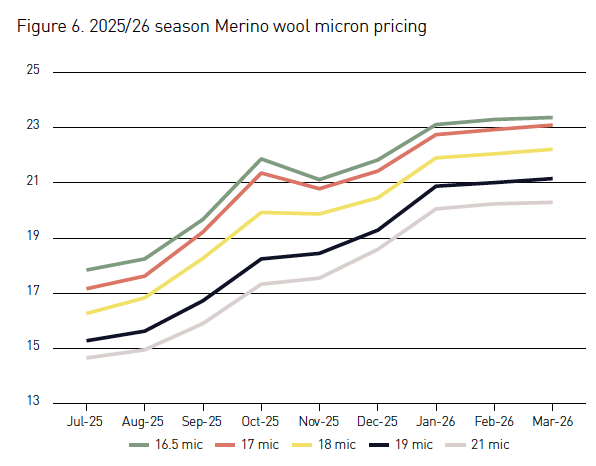

Since the start of the current season, Merino micron categories from 16.5–21 micron have recorded solid and well-supported gains. Prices lifted steadily through the early part of the season before accelerating sharply through September and October, with most microns adding around 300 to 400 cents per kilogram over that period. Following a brief consolidation in November, momentum resumed into December and January, with all microns finishing close to seasonal highs.

The strongest and most consistent gains have been evident in the core 18–21-micron range, which has improved by approximately 550 to 600 cents per kilogram season to date, reflecting strong demand for the main Merino types. On a percentage basis, 20-micron wool has been the standout performer, rising by 44%, and 19 micron at 39%. Finer microns have also lifted, with 17 micron up 35%, while 16.5 micron recorded the smallest increase at 31%.

As the Australian wool clip continues its longer-term shift finer, the price premium for superfine wool appears to be narrowing as supply increases. In contrast, medium-type Merino wools continue to perform strongly within a progressively finer national clip.

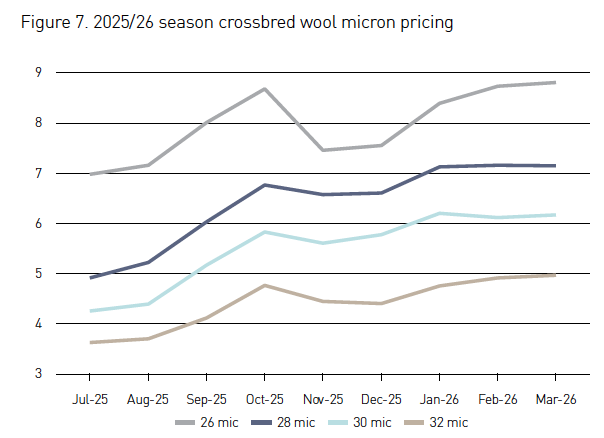

Over the past 12 months, the crossbred wool market has recorded solid price growth, largely rebounding from historically low levels. Over the last seven months, 30-micron wool has lifted by around 190 cents clean per kilogram, while 32-micron wool has improved by approximately 130 cents. On a percentage basis, 30-micron wool has recorded the strongest seasonal gain to date, rising by 45%, with 32-micron up 37%. The 28-micron category has seen more modest gains sitting 17 cents dearer. Based on AWEX average returns per head, a 5 kg 28-micron fleece at this time last year would have generated a gross return of around $13 per head. Today, the same fleece would return around $23 per head. Current returns mean many growers are likely now able to recover shearing costs from adult crossbred wool sheep.

Demand signals – Zhangjiagang Wool Industrial Association

During the 27th meeting of the Zhangjiagang Wool Industrial Association, industry leaders noted that recent wool price gains are increasingly being driven by underlying supply–demand fundamentals rather than sentiment. Feedback highlighted a sustained contraction in global wool production, now translating into tighter raw material availability and lower inventories across the supply chain. From a demand perspective, while early price rises in late 2025 were met with caution, subsequent increases were seen as more fundamentally driven and supported by genuine downstream demand. Processors also observed that downside risk for fine wool prices now appears limited, though there was broad recognition that a measured pace of price appreciation will be important to ensure the recovery remains sustainable.

This article appeared in Issue 105 of AWI’s Beyond the Bale magazine that was published in March 2026. Reproduction of the article is encouraged and should be attributed as follows: This article was first published in Issue 105 of AWI’s Beyond the Bale magazine.