Australian Wool Production Forecast Report April 2026

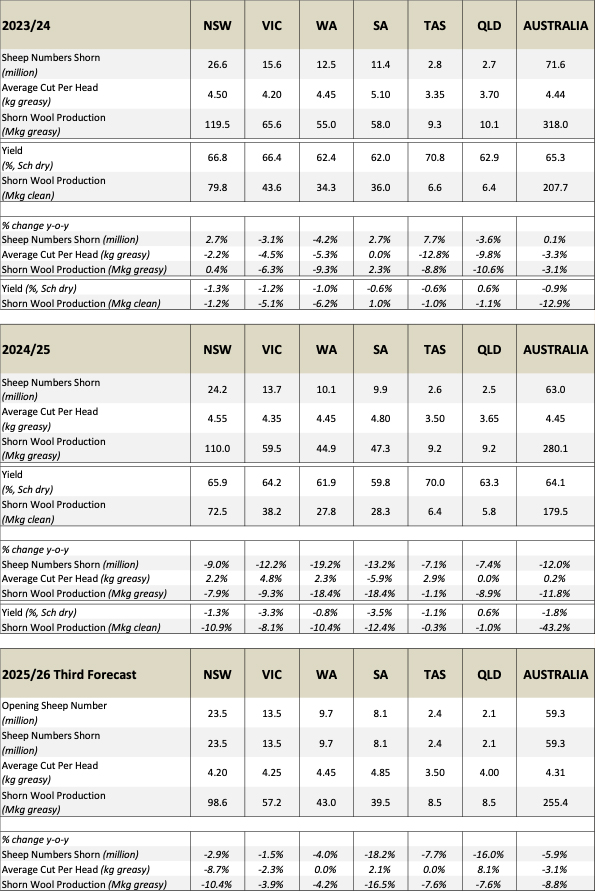

The Australian Wool Production Forecasting Committee’s (AWPFC) fourth forecast of shorn wool production for the 2025/26 season is 255.4 Mkg greasy. This is 8.8% lower than the 2024/25 season estimate.

Summary

- The Australian Wool Production Forecasting Committee’s (AWPFC) fourth forecast of shorn wool production for the 2025/26 season is 255.4 Mkg greasy. This is 8.8% lower than the 2024/25 season estimate.

- A year-on-year decline in shorn wool production in 2025/26 was forecast for all states ranging from down 16.5% in South Australia (39.5 Mkg greasy) to down 4.2% (43.0 Mkg greasy) in Western Australia. New South Wales is forecast to produce 98.6 Mkg greasy (down 10.2%) and Victoria 57.2 Mkg greasy (down 3.9%). Tasmania and Queensland are both forecast to produce 8.5 Mkg greasy (both down 7.6%).

- Average cut per head is forecast to be 4.31 kg greasy (down 3.1%). AWTA key test data for the 2025/26 season to the end of March show no change in mean fibre diameter (20.5 µm) or vegetable matter (2.2%), a 0.3 mm increase in staple length (88.1 mm), 0.6 N/ktex reduction in staple strength (32.8 N/ktex) and a 0.6% reduction in yield (64.1%).

- AWTA wool test volumes (greasy weight) for the 2025/26 season to the end of March were 208.5 Mkg greasy down by 9.5% on a year-on-year basis. AWEX data showed that firsthand wool offered at auction during 2025/26 to the end of March (week 40) were 197.3 kg greasy, down by 3.1%.

- Compared with the same time last year sheep and lamb slaughter from July to December 2025 were down 25% and 12% respectively. Looking at the 5-year (July to December) averages, sheep slaughter remained 12% higher and lamb slaughter 5% lower. Based on ABS slaughter numbers, both sheep and lamb weights were higher than in the December quarter in 2024.

- The Bureau of Meteorology’s outlook for May to July 2026 is for below average rainfall for most of Australia. For the coastal parts of NSW, south-east Qld and southern agricultural regions there is no clear signal for either wetter or drier conditions, meaning there are roughly equal chances of above or below average rainfall. There is an increased chance (>50%) of unusually low rainfall (in the driest 20% of April to June records between 1981 and 2018) for parts of south-eastern and interior Australia. Wamer than average days and nights are likely across most of Australia with a mixed outlook for overnight temperatures.

- The Australian Wool Production Forecasting Committee’s (AWPFC) first forecast of shorn wool production for the 2026/27 season is 243.9 million kilograms (Mkg) greasy. This is 4.5% lower than the 2025/26 fourth forecast.

- Table 1 summarises Australian wool production and Table 2 shows the total shorn wool production by state. Table 3 provides a comparison of AWTA key test data for the 2024/25 and 2025/26 seasons (July to November).

- The AWPFC adopted the ABS flock estimates released in December 2025, which included revised national flock figures from 2016/17 onwards that reflect the change in scope to capture all sheep grown for commercial gain in Australia.

Table 1: Summary of Australian wool production

Table 2: Total shorn wool production by state

Table 3: AWTA key test data for 2024/25 and 2025/26 (July to March)

- More detailed information on the shorn wool production by state in 2025/26 can be found in Table A1 in the Appendix to this report.

- The Appendix also provides historical data for Australia, including sheep shorn numbers, average cut per head and shorn wool production (Table A2) as well as the micron profile (Table A3) since 1991/92.

Detail on shorn wool production in 2025/26

Major data inputs

The AWPFC forecasts are based on detailed consideration by the state and national committees of data from various sources including:

- AWTA wool test data for the 2025/26 season July 2025 to March 2026;

- AWEX first-hand auction statistics for the 2025/26 season July 2025 to March 2026 (Week 40);

- ABS sheep and lamb turn-off for the 2025/26 season July to December 2025;

- Information on current and expected seasonal conditions from the Bureau of Meteorology.

AWTA wool test data

Every month AWTA releases data on the volumes of greasy wool tested within the various diameter categories for the month and the season to date. Data for the 2025/26 season July to March are compared with previous seasons (2021/22 to 2024/25) in this report.

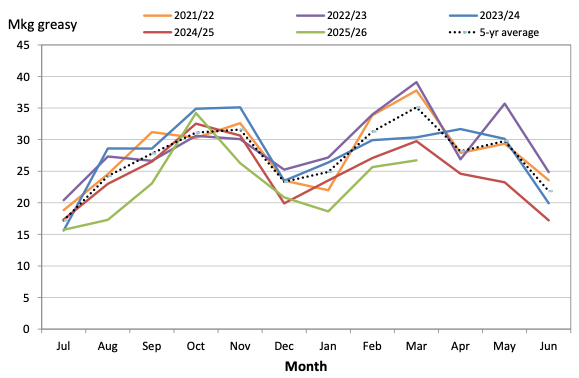

The month-by-month comparison of wool tested during the 2025/26 season July to March show test volumes below the past four seasons from July to September, November and January through to March. October 2025 test volumes were second only to October 2023 with 2024 and 2025 December test volumes very similar (Figure 1).

Figure 1: Comparison of monthly AWTA key test data volumes for the 2025/26 season with previous seasons (2021/22 to 2024/25) July to March. The dotted line represented the 5-year average (2020/21 to 2024/25).

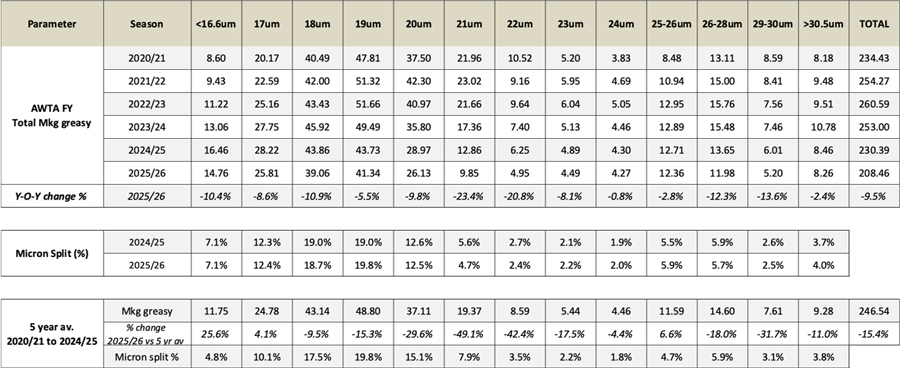

AWTA national wool test volumes data for the 2025/26 season July to March (Table 4) show:

- Volumes of wool tested were 9.5% lower than the 2024/25 season July to March at 208.46 Mkg greasy. This was 15.4% lower than the five-year average from 2020/21 to 2024/25 July to March.

- The weight of wool tested in all micron categories, decreased by between 0.8% (24 microns) and 23.4% (21 microns) compared with 2024/25 July to March.

- The largest micron categories by volume were the 19-micron (41.3 Mkg greasy), 18-micron (39.1 Mkg greasy) and 20-micron (26.1 Mkg greasy) categories.

- The micron split (% of total weight of wool tested) during 2025/26 July to March across the fibre diameter range was consistent with the 2024/25 season to March.

Table 4: AWTA key test data volumes (Mkg greasy) by micron range 2020/21 to 2025/26 July to March

Note: The micron categories refer to a range of -0.4 and +0.5um around each number. For example, 18um is between 17.6 and 18.5 microns.

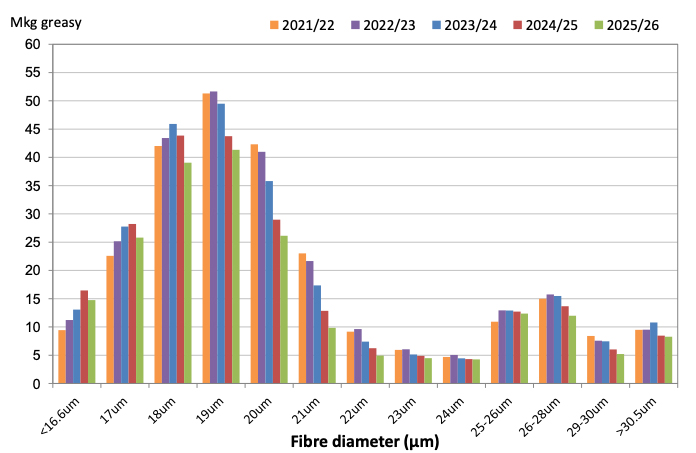

The micron profile of the Australian wool clip continues to have two distinct peaks. One centred around 18- to 19-micron wool (finer than 16.6 microns up to 23 microns) and a second centred around 26 - 28 microns (from 24 microns to 30.5 microns and broader) (Figure 2).

Figure 2: Australian fibre diameter profile – 2025/26 season compared with the 2021/22 to 2024/25 seasons July to March

A historical comparison of the Australian wool clip’s micron profile percentage share and average micron can be found in Appendix Table A3 (at the end of this report).

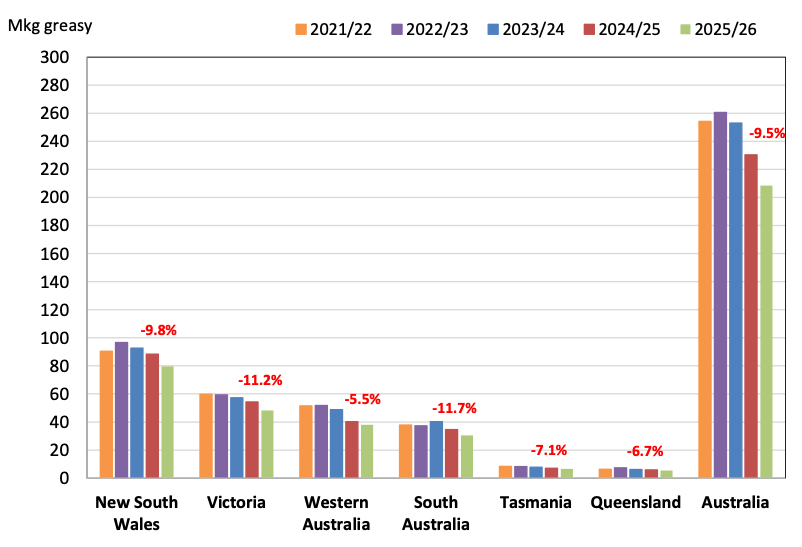

Based on data by Wool Statistical Area (WSA), the volumes of wool tested during 2025/26 July to November decreased in all states (Figure 3). South Australia had the greatest decrease in the volume of wool tested (down 11.7%), followed by Victoria (down 11.2%), New South Wales (down 9.8%), Tasmania (down 7.1%), Queensland (down 6.7%) and Western Australia (down 5.5%).

Figure 3: Volume of wool tested (AWTA WSA data) during the 2025/26 season compared with previous seasons (2021/22 to 2024/25) July to March. The percentage change in red font is the 2025/26 season compared with the 2024/25 season.

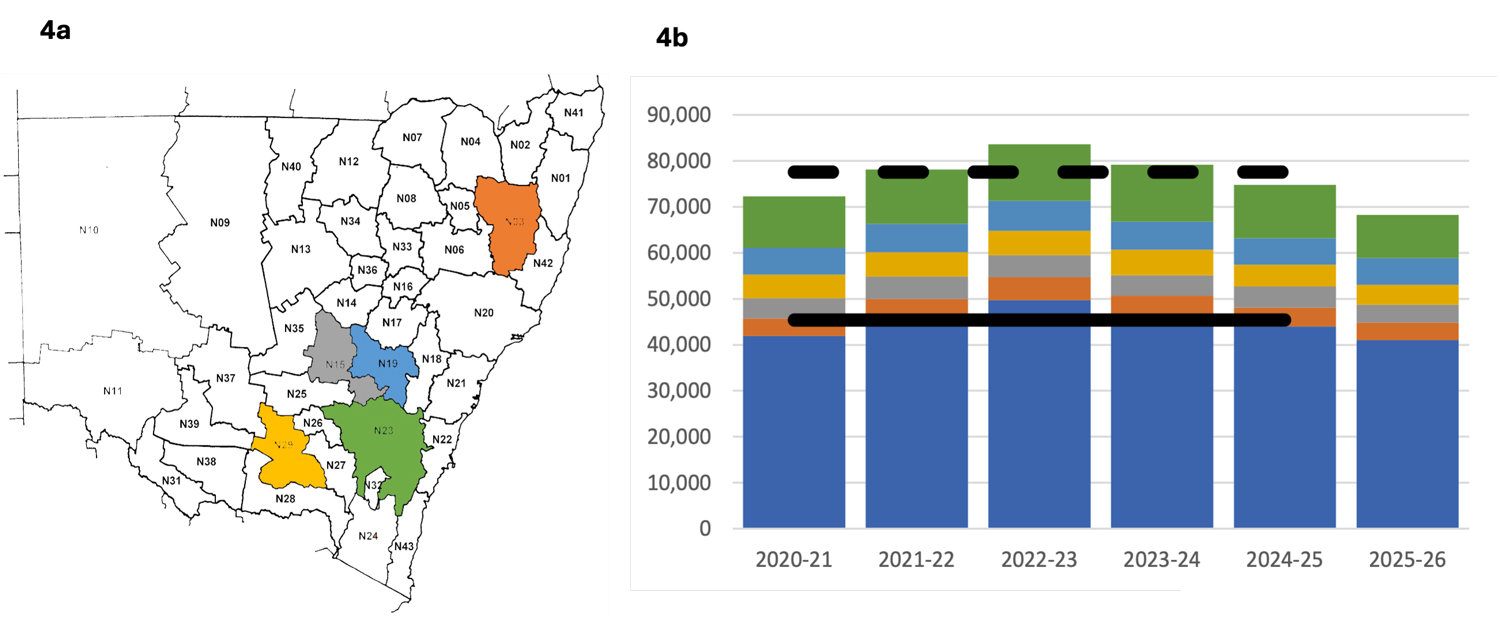

In New South Wales, the greatest volumes of wool tested originated from WSA regions N23 (13.8%), N19 (8.5%), N29 (6.4%), N15 (5.8%) and N03 (5.6%) (Figure 4a). Collectively, these five WSAs represented 39.9% of the total weight of wool tested in New South Wales during 2025/26 July to March (Figure 4b).

Figure 4a: The five New South Wales WSA regions from which the greatest volumes of wool tested originated and 4b: The total wool test volumes for the 2025/26 season compared with previous seasons (2020/21 to 2024/25) July to March. The larger blue portion of each column represents the other WSA regions with the coloured bars representing the 5 largest WSA regions: green; light blue; yellow; grey & orange. The continuous black horizontal line represents the 5-year average from 2020/21 to 2024/25 July to March for the other WSAs with the dashed black line the five-year average for the state. Data is in greasy tonnes.

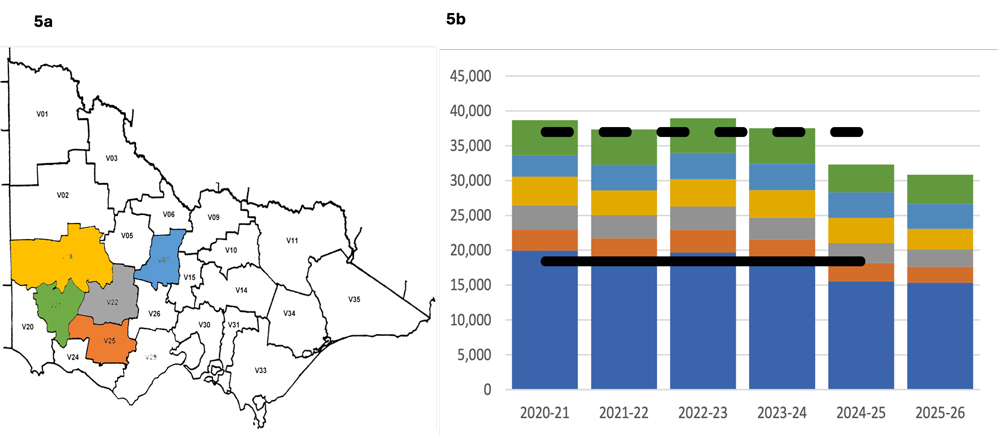

In Victoria, the greatest volumes of wool tested originated from WSA regions V21 (13.6%), V07 (11.5%), V18 (9.6%), V22 (8.1%) and V25 (7.3%) (Figure 5a). Collectively, these five WSAs represented 50.2% of the total weight of wool tested in Victoria during 2025/26 July to March (Figure 5b).

Figure 5a: The five Victorian WSA regions from which the greatest volumes of wool tested originated and 5b: The total wool test volumes for the 2025/26 season compared with previous seasons (2020/21 to 2024/25) July to March. The larger blue portion of each column represents the other WSA regions with the coloured bars representing the 5 largest WSA regions: green; light blue; yellow; grey & orange. The continuous black horizontal line represents the 5-year average from 2020/21 to 2024/25 July to March for the other WSAs with the dashed black line the five-year average for the state. Data is in greasy tonnes.

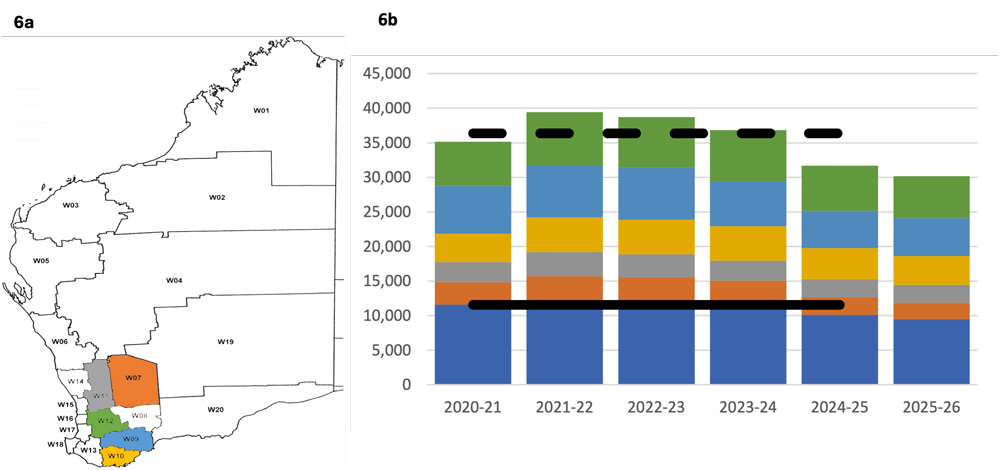

In Western Australia, the greatest volumes of wool tested originated from WSA regions W12 (20.0%), W09 (18.2%), W10 (13.9%), W11 (8.5%) and W07 (7.8%) (Figure 6a). Collectively, these five WSAs represented 68.5% of the total weight of wool tested in Western Australia during 2025/26 (Figure 6b).

Figure 6a: The five Western Australian WSA regions from which the greatest volumes of wool tested originated and 6b: The total wool test volumes for the 2025/26 season compared with previous seasons (2020/21 to 2024/25) July to March. The larger blue portion of each column represents the other WSA regions with the coloured bars representing the 5 largest WSA regions: green; light blue; yellow; grey & orange. The continuous black horizontal line represents the 5-year average from 2020/21 to 2024/25 July to March for the other WSAs with the dashed black line the five-year average for the state. Data is in greasy tonnes.

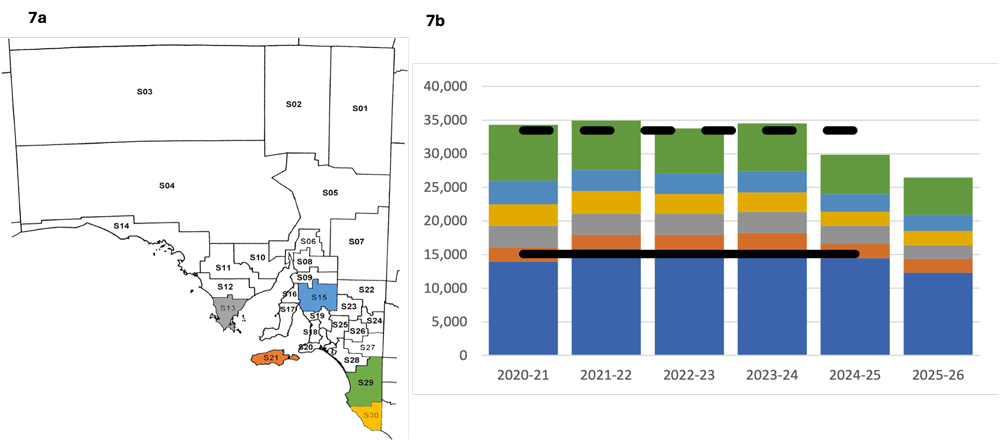

In South Australia, the greatest volumes of wool tested originated from WSA regions S29 (20.9%), S15 (9.1%), S30 (8.1%), S13 (7.8%) and S21 (7.7%) (Figure 7a). Collectively, these five WSAs represented 53.5% of the total weight of wool tested in South Australia during 2025/26 July to March (Figure 7b).

Figure 7a: The five South Australian WSA regions from which the greatest volumes of wool tested originated and 7b: The total wool test volumes for the 2025/26 season compared with previous seasons (2020/21 to 2024/25) July to March. The larger blue portion of each column represents the other WSA regions with the coloured bars representing the 5 largest WSA regions: green; light blue; yellow; grey & orange. The continuous black horizontal line represents the 5-year average from 2020/21 to 2024/25 July to March for the other WSAs with the dashed black line the five-year average for the state. Data is in greasy tonnes.

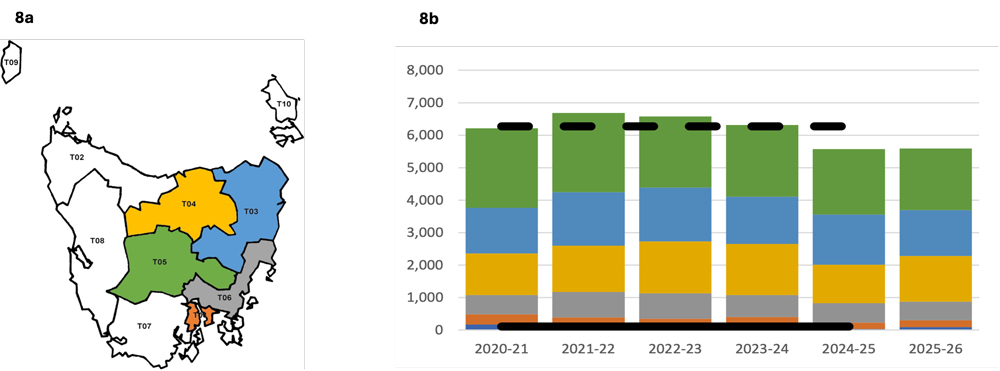

In Tasmania, the greatest volumes of wool tested originated from WSA regions T05 (33.9%), T03 (25.2%), T04 (25.2%), T06 (10.3%) and T01 (3.8%) (Figure 8a). Collectively, these five WSAs represented 98.4% of the total weight of wool tested in Tasmania during 2025/26 July to March (Figure 8b).

Figure 8a: The five Tasmanian WSA regions from which the greatest volumes of wool tested originated and 8b: The total wool test volumes for the 2025/26 season compared with previous seasons (2020/21 to 2024/25) July to March. The larger blue portion of each column represents the other WSA regions with the coloured bars representing the 5 largest WSA regions: green; light blue; yellow; grey & orange. The continuous black horizontal line represents the 5-year average from 20120/21 to 2024/25 July to March for the other WSAs with the dashed black line the five-year average for the state. Data is in greasy tonnes.

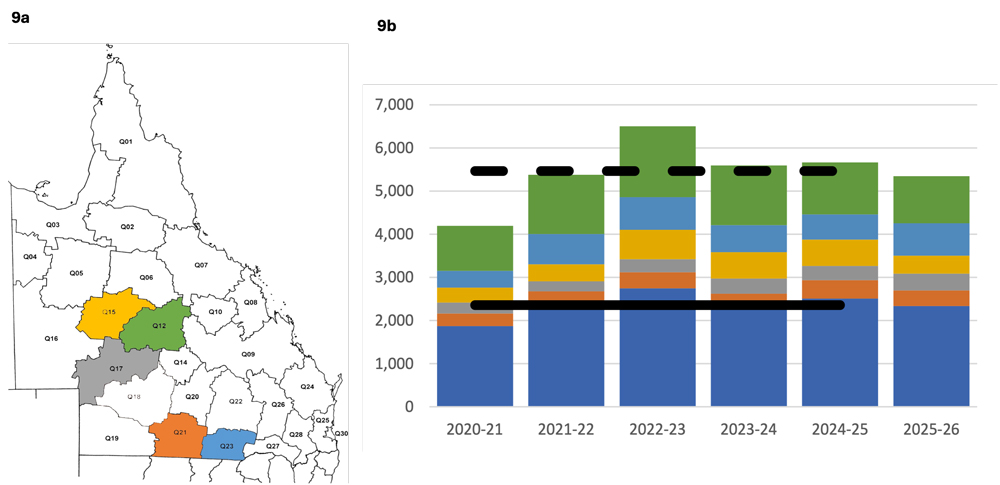

In Queensland, the greatest volumes of wool tested originated from WSA regions Q12 (20.4%), Q23 (14.0%), Q15 (7.9%), Q17 (7.2%) and Q21 (6.8%) (Figure 9a). Collectively, these five WSAs represented 56.3% of the total weight of wool tested in Queensland during 2025/26 July to March (Figure 9b).

Figure 9a: The five Queensland WSA regions from which the greatest volumes of wool tested originated and 9b: The total wool test volumes for the 2025/26 season compared with previous seasons (2020/21 to 2024/25) July to March. The larger blue portion of each column represents the other WSA regions with the coloured bars representing the 5 largest WSA regions: green; light blue; yellow; grey & orange. The continuous black horizontal line represents the 5-year average from 2020/21 to 2024/25 July to March for the other WSAs with the dashed black line the five-year average for the state. Data is in greasy tonnes.

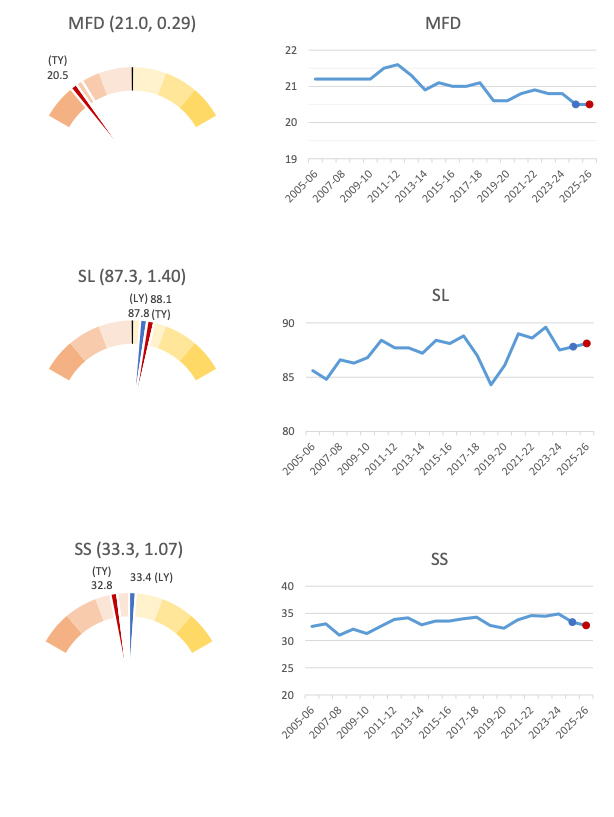

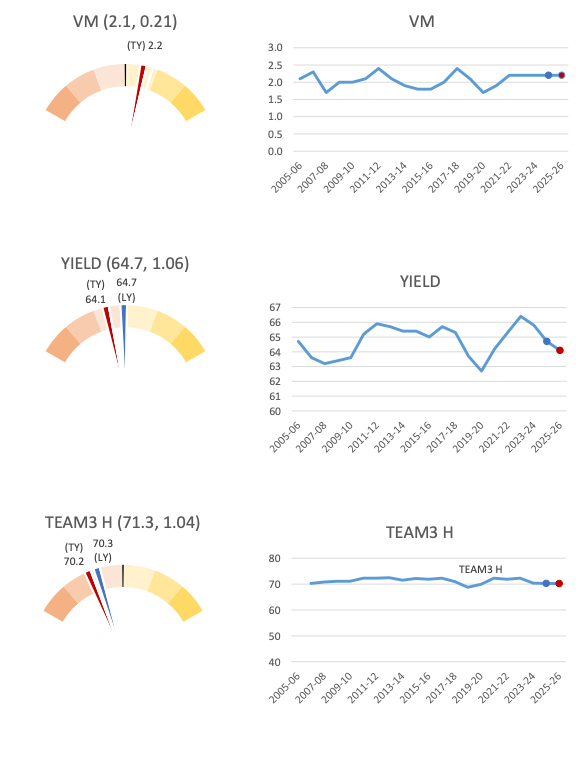

A graphical representation of the AWTA Key Test Data changes in mean fibre diameter (MFD), vegetable matter (VM), staple length (SL), yield (YIELD), staple strength (SS) and hauteur (TEAM 3 H) from the 2005/06 to the 2025/26 season July to March is shown in Figure 10. On each graph the red dot represents the mean value of each characteristic for the 2025/26 season while the blue dot represents the mean for the 2024/25 season July to March. The values above the gauge on the left-hand side of each graph show the mean and standard deviation respectively for that characteristic from 2005/06 to 2025/26. Each coloured segment on the gauges represents one standard deviation with the mean at 12 o-clock (centre). For MFD, VM, SL, YIELD and SS, the mean and standard deviation are based on data from the 2005/06 season onwards. For TEAM 3 the mean and standard deviation are based on data from the 2006/07 season onwards. The red line on each gauge is the mean for the 2025/26 season (TY), while the blue line is the mean for the 2024/25 season (LY) July to March.

- On a national basis, compared with the 2024/25 season July to March, mean fibre diameter was unchanged at 20.5 microns, staple length was up 0.3 mm to 88.1 mm and staple strength was down 0.6 N/ktex to 32.8 N/ktex (Figure 10a).

- Vegetable matter was unchanged at 2.2%, yield was down 0.6% to 64.1% and predicted hauteur (TEAM 3) was down 0.1 mm to 70.21.5 mm (Figure 10b).

Figure 10a: AWTA Key Test Data mean fibre diameter (MFD), staple length (SL) and staple strength (SS) for the Australian wool clip from 2005/06 to 2025/26 July to March

Figure 10b: AWTA Key Test Data vegetable matter (VM), yield (YIELD) and TEAM 3 H (TEAM 3 H) for the Australian wool clip from 2005/06 to 2025/26 July to March

AWEX auction statistics

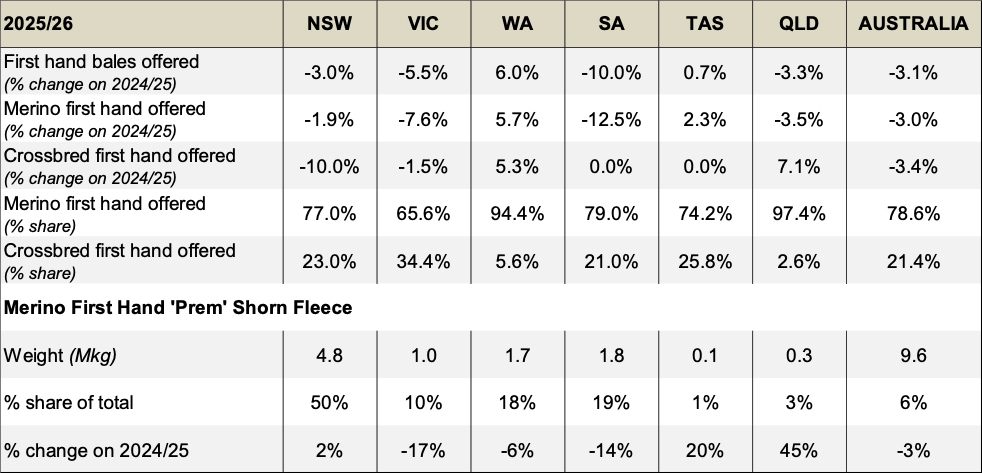

The volume of AWEX first-hand auction lots offered for the 2025/26 season July to March was 197.3 Mkg greasy. This was 3.1% lower than the same time in 2024/25 (Table 5).

Table 5: AWEX Auction National Volumes (Mkg greasy): 2023/24 to 2025/26 (July 2025 to March 2026 – Week 40)

- First-hand bales offered decreased in all states, except Western Australia which increased by 6.0% and Tasmania by 0.7%. South Australia had the greatest decrease (down 10.0%), followed by Victoria (down 5.5%), Queensland (down 3.3%) and New South Wales (down 3.0%) (Table 6).

- The volume of first-hand Merino wool offered across Australia between July to March 2025 decreased by 3.0% compared with 2024/25 with the volume of first-hand Crossbred wool offered down 3.4%. The share of Merino wool of all first-hand offered wool was 78.6% in both 2025/26 and 2025/25 July to March, compared with 77.8% in 2023/24 July to March.

- There was a 3% decrease in the volume of ‘Prem-shorn’ Merino fleece wool in 2025/26 (9.3 Mkg greasy) compared with 2024/25 (9.9 Mkg greasy).

- As a percentage share of the total first-hand wool offered, 6% of Australian first-hand bales offered were prem shorn in 2025/26 July to March. On a state-by-state basis this ranged from 1% in Tasmania to 50% in New South Wales

Table 6: AWEX first-hand auction statistics 2025/26 compared with 2024/25 July to March

Note: Data on ‘prem shorn’ wool from AWEX is based on the assessed length of the wool being offered. It is defined as <85 - 75 mm, depending on micron and excluding weaners and lambs wool

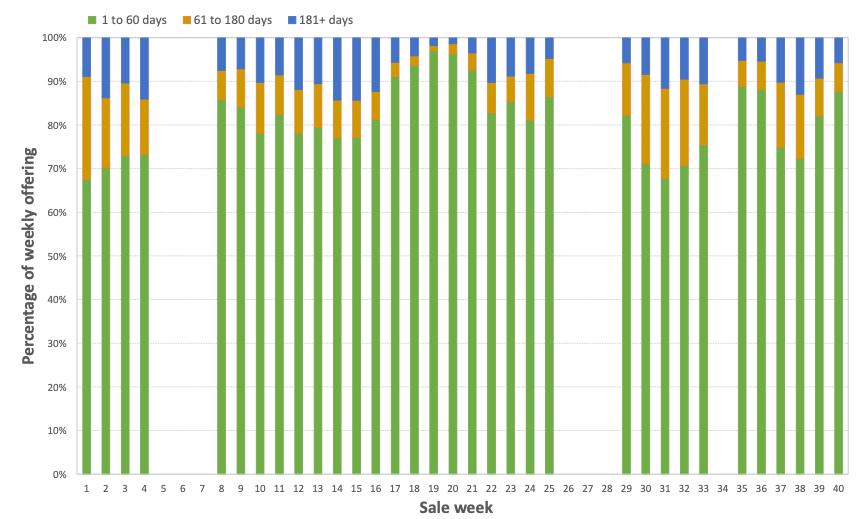

AWEX auction volumes during 2025/26 to March have included wool shorn in previous seasons. Some catalogues have contained up to 30% older bales that were tested with 61 -180 and more than 181 days since they were tested (Figure 11).

Figure 11: AWEX Age profile days since tested (bales) 2025/26 season (to week 40). The numbers surrounding the green line represent the percentage of the weekly offering that was tested between 1 and 60 days prior to sale

Australian Bureau of Statistics (ABS) data

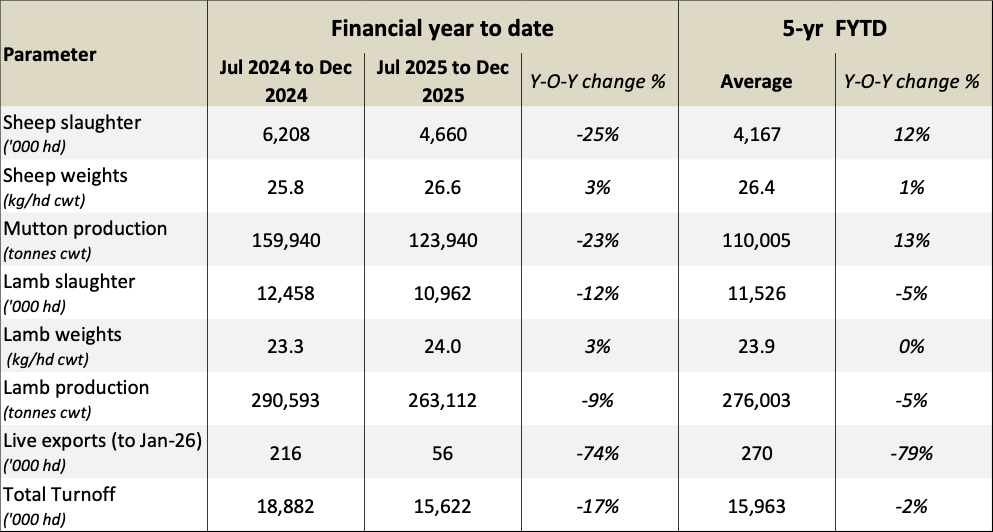

Australian sheep and lamb turn-off statistics during 2025/26 July to December are shown in Table 7:

- There was a 25% decrease in sheep slaughter, and a 12% decrease in lamb slaughter compared with July to December 2024/25.

- Sheep slaughter was 12% above the five-year average with lamb slaughter 5% lower than the five-year average.

- Total turnoff of sheep and lambs for 2025/26 July to December was 17% lower than 2024/25 and 2% below the five-year average.

Table 7: ABS Sheep turn-off data for 2025/26 compared with 2024/25 July to December

Bureau of Meteorology (BoM) seasonal rainfall seasonal outlook

Rainfall deciles during 2025/26 July to March were average to very much above average in Western Australia and in the key wool producing regions of South Australia. Rainfall deciles were above very much above average in northwest New South Wales and above average in central Queensland. In the remaining starts rainfall deciles ranged from very much below average to average (Figure 12).

Figure 12: Australian rainfall deciles, 2025/26 season July to November. Source: Bureau of Meteorology

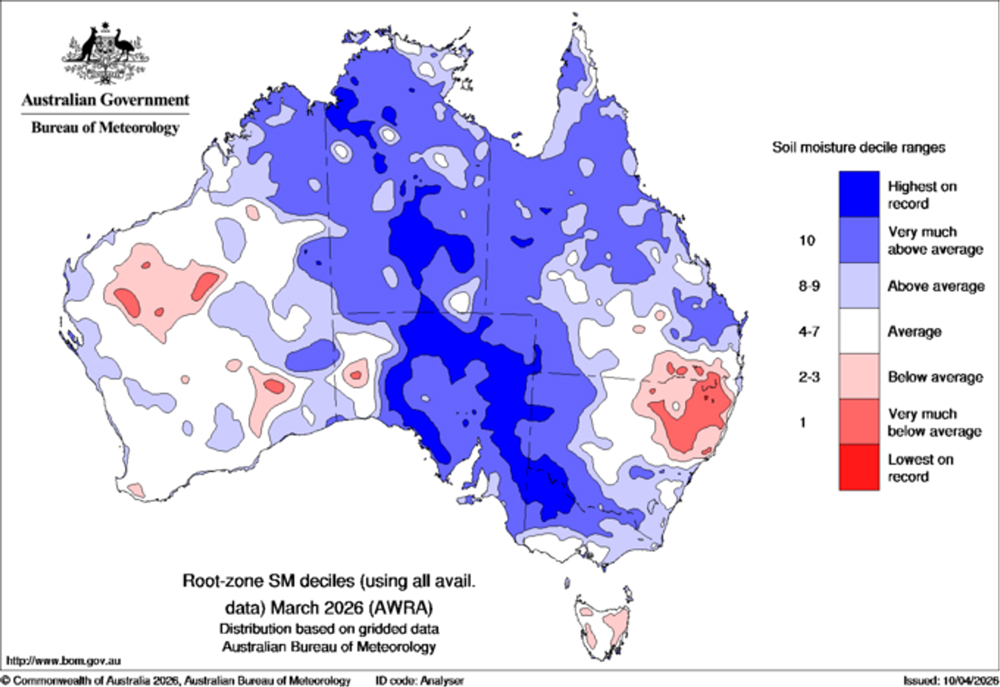

The root-zone soil moisture deciles for November 2025 reflect the seasonal conditions and rainfall between July and March (Figure 13).

Figure 13: Australian root-zone soil moisture deciles November 2025. Source: Bureau of Meteorology

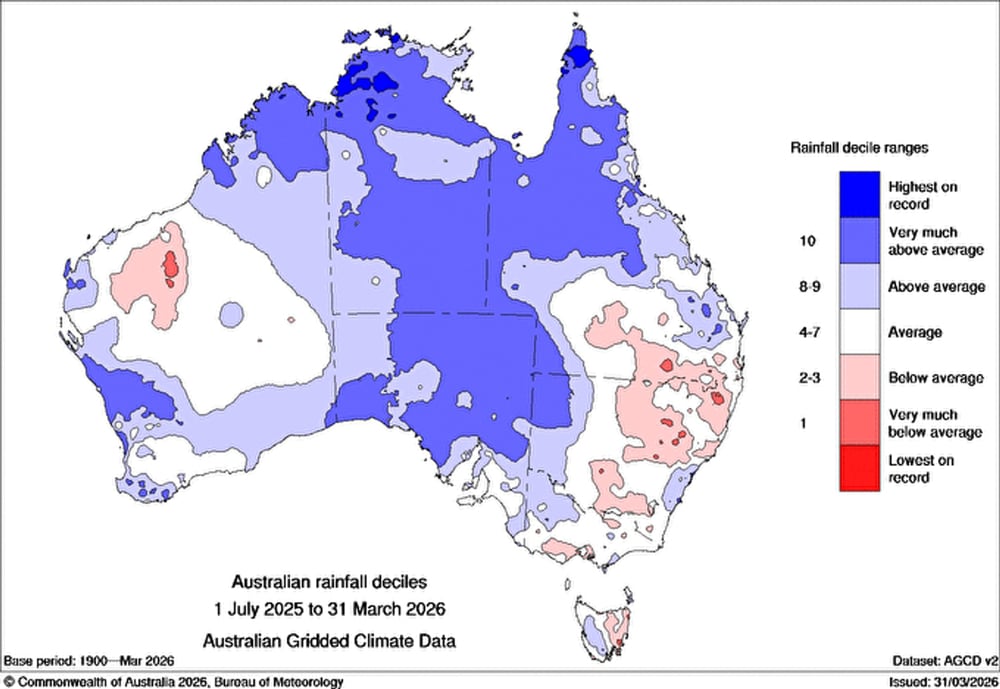

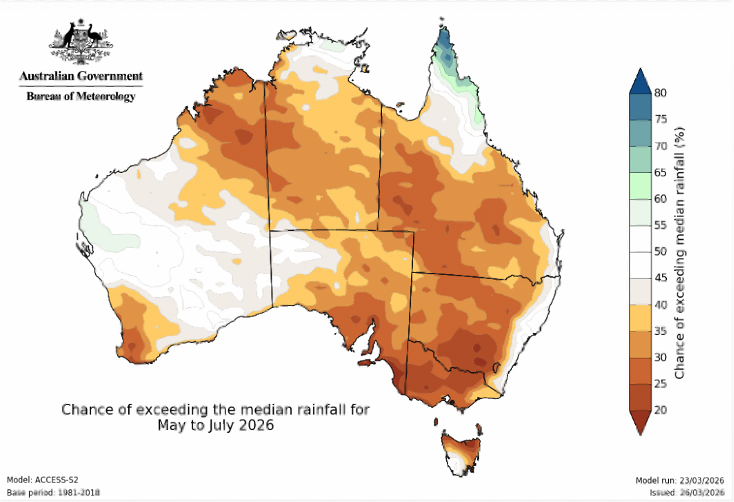

The Bureau of Meteorology’s outlook for May to July 2026 is for below average median rainfall for most of Australia. Rainfall over April to June is likely to be below average (60% to more than 80% chance) for most of Australia. For the coastal parts of NSW, south-east Qld and southern agricultural regions there is no clear signal for either wetter or drier conditions, meaning there are roughly equal chances of above or below average rainfall. There is an increased chance (>50%) of unusually low rainfall (in the driest 20% of April to June records between 1981 and 2018) for parts of south-eastern and interior Australia (Figure 14).

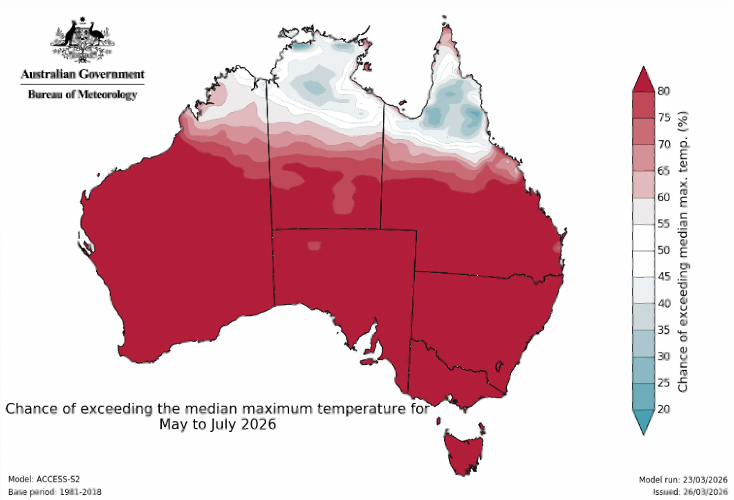

Maximum temperatures for April to June are very likely to be above average (more than 80% chance) across the southern two-thirds of Australia. The southern half of Australia has an increased chance (>50%) of unusually high maximum temperatures. The strongest chances in western parts of WA, eastern NSW and Tas, and north-eastern Vic (over 80% chance). Minimum temperatures are likely (60% to greater than 80% chance) to be above average across much of the eastern states and most of WA. For most remaining inland and north-western areas of Australia, there is no clear signal for either warmer or cooler than average minimum temperatures. There is an increased chance of unusually high minimum temperatures (>50% chance) for parts of WA's south and west, the coastal strip extending from southern Qld to eastern Vic, and much of Tas (warmest 20% of April to June days and nights, respectively, between 1981 and 2018). (Figure 15).

Figure 14: Chance of exceeding median rainfall (May to Jul-26)

Figure 15: Chance of exceeding median maximum temperature (May to Jul-26)

State Committee input

The following provides a summary of seasonal conditions and the wool production estimate for 2025/26 as reported by the AWPFC state committees in April 2026.

New South Wales

2025/26 season. Bureau of Meteorology rainfall deciles for the 2025/26 season to March show highest on record for the northwest corner of the state and above average for the southwestern region but average to below average in key wool producing regions (N23, N19, N29, N15 and N03). This was reflected in average soil moisture levels through most of the state to below average and lowest on record in the northeast region. The Northern Tablelands region is extremely dry, sheep and cattle yardings in recent months have been very high. Demand from restockers in the Northern Tablelands is virtually non-existent, sheep numbers in that region are expected to be well down. Few stock feed crops have been planted in northern regions. A very patchy season throughout the remainder of the state, but most areas are tending dry to very dry. An early break with reasonable rain in some southeastern regions (Central Tablelands, Southern Tablelands and into eastern parts of the Riverina) and warmer temperatures have triggered pasture growth but follow-up rain is now required. Further hot and windy conditions will put the existing feedbase under increasing pressure.

Availability of stock water, particularly for properties reliant on dams, is an ongoing issue. Stock (sheep and cattle) are moving to agistment in the northwest region to make use of abundant feed. Dry ewes and wethers have been sold in the central west and western agricultural regions earlier than usual (many without shearing), with producers focusing on feeding their breeding ewes. Wether lambs that would normally be shorn and held will be sold as stores. Some reports of producers in mixed farming regions opting not to join. In eastern regions with sufficient feed, producers are looking to restock but the cost of buying in sheep is a key issue.

In mixed farming regions, some reports of fewer hectares sown to cereals or oilseeds due to fuel and urea availability concerns, with multi-species pastures of grazing crops as a substitute. These properties will be looking for sheep in the new season. Other regions have enough fuel and urea to make a start on their cropping program but are unsure whether they will be able to complete their planned program. The next 3 to 4 weeks will be critical for these decisions.

Some long-stored on-farm wool clips have come into store in response to the higher wool prices since October 2025, particularly from mixed farming regions. This may have increased the AWTA wool test volumes. Only the finer end of the micron range (≤ 17.5 µm) showed a year-on-year increase in testing volumes, indicative of the poor season across most of the state. AWTA key test data show little year-on-year change, MFD down 0.1 μm to 20.4 μm, SL down 0.1 mm to 86.6 mm, SS down 1.2 N/ktex to 34.9 N/ktex VM up 0.1% to 2.7% and yield down 1.2% to 69.6%. The New South Wales Committee’s fourth forecast of shorn wool production for 2025/26 is 98.52 Mkg greasy, down 10.4% on 2024/25.

2026/27 season. The Committee reduced the opening numbers for 2026/27 due to fewer ewes expected to be joined in 2025/26, expected lower lambing and marking percentages and increased turnoff of older ewes. The sheep shorn numbers were reduced to account for sheep sold for processing in the wool during 2025/26.

Positive producer sentiment is expected to continue given the high wool and sheep meat prices. But the season will be the key factor limiting shorn wool production. The New South Wales Committee’s first forecast of shorn wool production for 2026/27 is 93.54 Mkg greasy, down 5.1% on 2025/26.

Victoria

2025/26 season. Bureau of Meteorology rainfall deciles for the 2025/26 season to date show average to above average for most of the state, except for V24 and parts of V25 and V29. Soil moisture deciles to end of February mirrored the rainfall deciles. Positive changes to the season across most of the state since the December meeting. October rains produced some decent feed, but that did cut out over summer. Northern Victoria and Gippsland regions are looking very good. In the southwest the pastures look green, but quantity is lacking. Feed costs have reduced in many regions.

Water availability remains a critical factor for most of Victoria, particularly south of Bendigo to the South Australian border. Properties that rely on run off and dam water for stock are still carting water. Further rainfall (>25 mm) is required to replete on-farm storages. The quantity and quality of groundwater is also becoming an issue.

Bushfires south of Bendigo impacted shearing sheds and other sheep infrastructure (n = 35,807 sheep lost) during January. Bigger producers are likely to re-build, smaller operations may switch to a different enterprise.

Lower sheep numbers on farm in many regions, but few sheep being sold at present. High sheep meat value has seen remaining older wethers sold. Few wethers remain available for sale. Dry ewes were sold at the end of 2025, they were sold in the wool if less than 40mm fleece due to high skin value ($24 - $27). Ewes with 6 months wool were shorn prior to sale. Some reports of producers buying joined ewes to build numbers, most producers remain conservative and are maintaining lower numbers.

Flocks joining in late November and December reaped the benefit of fresh pasture with good conception rates and scanning percentages. Lambing for those flocks has commenced with mild conditions to mid-April favourable for lamb survival. An early autumn break has set up later joining flocks (February – March) for good conception rates. Scanning contractors report that sheep are in good condition.

Fleece weights range from between ½ kg lower to on par with last season due to six months of good feed. Shearing teams are very quiet, a 10-day run is typically down to 7-days. Teams have moved interstate to chase work. Currently no lag between shearing and clips transported to store for testing and sale. AWTA key test data show little year-on-year change, no change in MFD at 21.4 μm (a 20-year low), SL down 0.3 mm to 88.5mm, SS down 1.5 N/ktex to 32.6 N/ktex, VM up 0.1% to 2.1% (a 20-year high) and yield down 1% to 63.8%. The Victorian Committee’s fourth forecast of shorn wool production for 2025/26 is 57.18 Mkg greasy, down 3.9% on 2024/25.

2026/27 season. The Committee expects fewer ewes were joined in 2025/26 as older ewes were sold with similar marking percentages from fewer sheep (i.e. lower stocking rate) and improved ewe conditions Fleece weights are expected to be higher. Further rain is required to the end of Autumn and into Winter to build the feedbase, replenish water storage and build producer confidence. Availability of superphosphate, nitrogen, pasture seed and lime is limited. This may reduce feed growth. Producers who had not applied fertiliser in previous season and were looking to do so now, may not be able to. The Victorian Committee’s first forecast of shorn wool production for 2026/27 is 50.33 Mkg greasy, down 12.0% on 2025/26.

Western Australia

2025/26 season. Bureau of Meteorology rainfall deciles were average to above average for the key wool producing regions (W12, W09, W10, W11 and W07) with soil moisture deciles following the same trend. The break of the season has occurred for most of the agricultural regions. Northern regions remain dry, but fewer sheep are run there. Follow up rain is now required.

Producer sentiment is variable. Some producers continue to exit the industry, taking advantage of the high sheep meat prices. Cropping is expected to decrease due to high input costs, which may prompt some enterprises to run sheep. Inquiries for breeding ewes have lifted in recent months, however buy in costs are a barrier. For areas that have sown crops, access to fertiliser and urea may be problematic to finish the crop.

Some reports of producers joining more ewes or purchasing from trade sales (moving into the wheatbelt and Esperance). Early pregnancy scanning results were average, winter lambing flocks will scan in the next 2 months. Increased focus on ewe lamb joinings to increase flock productivity. Some reports of dry ewes being remated to produce a late drop of lambs, generally with a terminal breed over a Merino. Crossbred joinings appear to be increasing to capture the current high value for a first-cross ewe from eastern states. Overall sheep numbers are expected to hold steady, most flock reduction occurred between October and December 2025.

AWTA key test data show year-on-year increases (MFD up 0.4 μm to 19.2 μm, SL up 2.7 mm to 89.0 mm, SS up 2.0 N/ktex to 30.1 N/ktex, no change in VM at 1.8% and yield up 1.1% to 63.6%) suggesting higher fleece weights. AWTA test volumes were bolstered by on-farm stored wool bought in for sale during January and February from mixed farming enterprises. Freshly shorn wool is being tested and offered for sale straightway. Producers have been happy to sell at recent price levels, reducing on-farm stocks. The bulk of the WA shearing is now completed; AWTA and regional stores are expecting wool test volumes to decrease to the end of the season. A few core lines have reduced from 5- to 4-days per week.

Abattoirs have been actively sourcing from trade sheep sales to bolster numbers. Eastern states buyers have been active in WA and paying higher or equivalent prices to the eastern states. Interstate transfers have been 90% lambs with most feedlot lambs. March to April lamb movements are also expected to be high. Fewer adults are being moved out of the state. The Western Australian Committee’s fourth forecast of shorn wool production for 2025/26 is 43.05 Mkg greasy, down 4.2% on 2024/25.

2026/27 season. The Committee reduced the number of ewes joined in 2025/26 due to fewer Merino hoggets in the state due to reduced Merino x Merino joinings in 2024, and increased interstate transfers as 339,000 head had passed through the Ceduna checkpoint to the end of February 2026. The 2025/26 marking rate was increased as dry ewes were re-joined to build numbers. The Western Australian Committee’s first forecast of shorn wool production for 2026/27 is 42.85 Mkg greasy, down 0.5% on 2025/26.

South Australia

2025/26 season. Very much above average to highest on record Bureau of Meteorology rainfall deciles for February and March 2026 in key wool producing regions has turned the season in those areas. Rain has continued into April, with most regions experiencing an autumn break. Excessive rain in northern regions has increased fly activity and flystrike. Producers responded quickly, mustering mobs and treating sheep. Some localised reports of creek and road damage impacting shearing on some properties. Producers who had intended to reduce numbers are now looking to hold them. Northern pastoral regions are now set up for a good two years. Some regions remain dry (i.e. Loxton), but they tend to have fewer sheep. The southeast has recovered well following some rain in September with lambing commencing in February and March. Feedbase has recovered in many regions.

High mutton prices continued to prompt sale of adult sheep prior to February. Reports of sheep sold in the wool due to high skin price ($16 - $20 for a Merino pelt). Lambs have been sold as stores ($200 to $220) rather than to processors, with sheep feed lotters active in the market and sourcing sheep from Western Australia.

Sheep numbers remain low, but producer sentiment has changed since December. Producers are keen to restock, but high restocker prices ($300 to $350) are a hindrance. Available feed is a key factor for many producers; some are taking the opportunity to allow their feedbase to grow before they buy in stock and are holding numbers for the short term. Cash flow is an important front of mind factor.

Higher wool prices have stalled further shifts to shedding breeds, with some Merino enterprises reverting to six- or eight-monthly shearing.

Concerns regarding fuel and fertiliser, may reduce cropping areas planted in favour of sheep production. However, banks are increasingly seeking returns on recently purchased cropping machinery. That and removal of sheep fencing and other infrastructure to increase arable paddock sizes may hamper any large move away from cropping.

Scanning rates have been very good in southern regions, despite the dry as producers have been able to manage ewe feed requirements. Some pastoral scanning rates are low, as ewes were in poor condition prior to joining. Some pastoral producers have re-joined or are considering re-joining which will produce several late lambing mobs.

AWTA key test data show little year-on-year change, MFD down 0.1 µm to 20.3 µm (a 20-year low), SL down 0.1 mm to 89.2mm, SS down 0.8 N/ktex to 32.0 N/ktex, VM down 0.3% to 2.6% and yield down 0.8% to 59.7% (also a 20-year low). AWTA test volumes were inflated by long-held on-farm stored wool coming onto the market from mixed farming regions. The South Australian Committee’s fourth forecast of shorn wool production for 2025/26 is 39.53 Mkg greasy, down 16.5% on 2024/25.

2026/27 season. The Committee expects the new season to be closer to average with improved sheep producer sentiment set to continue. The improved season in the last quarter of 2025/26 prompted the Committee to increase opening numbers by lifting the 2025/26 marking rate and reducing outbound interstate transfer. Fleece weights were expected to increase due to lower stocking rates. Despite this, lower sheep numbers will limit any increase in shorn wool production. The South Australian Committee’s first forecast of shorn wool production for 2026/27 is 39.52 Mkg greasy, no change on 2025/26.

Tasmania

2025/26 season. Bureau of Meteorology rainfall deciles for the season to date and soil moisture deciles (to Feb-26) show below average conditions in key wool producing regions. There have been several false starts but no autumn break following an ordinary winter, particularly in southern regions of the state, with some frost events. Rain is needed in the next few weeks to encourage feedbase growth prior to winter. The outlook for the remainder of 2025/26 is ordinary, particularly in southern regions. In northern regions producers have been sowing new pasture and forage crops, this is later than normal due to low soil moisture.

Mutton prices and the poor season have prompted sheep producers to turn off surplus stock. Sheep slaughter (Jul-Dec 25) was 3% lower year-on-year but 62% higher than the five-year average. Joining is currently underway. Sheep numbers are expected to hold to the end of June as the March quarter is not generally a turn-off period.

AWTA key test data show little year-on-year change, MFD down 0.1 µm to 20.6 µm, no change in SL (88.9mm), SS up 1.0 N/ktex to 36.8 N/ktex VM up 0.2% to 1.0% and yield down 0.8 to 69.6%. Average cut per head at 3.50 kg greasy as the reduced per head production due to the poor season was offset by the lower yield.

Monthly AWTA wool test volumes are tracking below the past 4 seasons and are expected to remain low to the end of June. 6.59 Mkg greasy have been tested to the end of March 2026. The Committee expect lower volumes to be tested between April and June 2026 (i.e. < 2 Mkg) than in previous seasons. High skin prices prompted sheep (mutton and lambs) to be processed without shearing. AWEX auction volumes have been increased with wool shorn in previous seasons. Some recent catalogues have contained 30% older bales (i.e. 61 -180 and >180 days since testing). The Tasmanian Committee’s fourth forecast of shorn wool production for 2025/26 is 8.54 Mkg greasy, down 7.1% on 2024/25.

2026/27 season. Producer confidence is reasonably high given market prices for wool and sheep meat. However, the poor seasonal outlook (drier and warmer) may lead to some producers reducing sheep numbers following scanning based on the numbers they will be able to lamb down with an expected feed shortage leading into winter. Fertiliser shortages and fuel prices are expected to have an impact on enterprise mix, potentially benefitting sheep production. The Tasmanian Committee’s first forecast of shorn wool production for 2026/27 is 8.69 Mkg greasy, up 1.8% on 2025/26.

Queensland

2025/26 season. Bureau of Meteorology rainfall deciles for the season to date show average to above average for central western region, with average to below average in southern and eastern regions with soil moisture deciles mirroring this rainfall pattern. The season is good north of Mitchell and Charleville, as well as around Blackhall and Isis but drier further south and east particularly near the New South Wales border. For the latter, dams are empty and properties destocked. Around Longreach the season is patchy, as late winter rain decreased feedbase quality.

Many producers were feeding through to October and November, have had good conception rates and are beginning to lamb now. Sheep weights are increasing, with some fattened wether lambs being sold (either autumn or May/June 2025 lambing). Dry ewes are also being sold.

The transition to shedders has appeared to have stabilised, with fewer producers now talking about making the change. Merino numbers are expected to stabilise due to increased producer sentiment from higher wool and sheep meat prices. No dramatic increase in numbers is expected, with some larger producers are increasing wether numbers on the back of a good season, although high lamb prices may temper this. Smaller consignments from individual properties are being sent for sale in New South Wales, producers are taking the opportunity to clear out small numbers of stock they would normally dispose of by other means. This highlights the lower number of sheep on-farm in Queensland.

Wild dogs remain a concern in many areas, even in those where flood-damaged exclusion fencing has been repaired as dogs were inside the fencing when repairs were complete. Active trapping is underway. Pigs are another on-going concern. Labour availability remains an issue.

The feedbase is being impacted by African Lovegrass, particularly in lighter regions, and dieback in buffel grass in others. While many properties have maintained their focus on goats, degradation of pasture and reduced processing capacity may have produced a peak in goat production in Queensland. Some goat producers may swing back into meat sheep.

Wool cuts are expected to be higher, particularly in the key central west region as a follow on from the floods and due to the high turn-off of lambs with lower fleece weights. Some clips have come in substantially larger (i.e. higher number of bales) than expected. AWTA key test data show little year-on-year change, MFD down 0.1 μm to 19.0 μm (a 20-year low), SL down 0.4 mm to 88.1 mm, SS down 0.8 N/ktex to 34.8 N/ktex, VM down 0.2% to 3.2% and yield up 1% to 64.3%.

Massive decline in on-farm wool stocks and sell down due to the increase in the wool market. Wool growers who normally sell after 1 July have sent their wool in for sale over March/April, with other expected to do so in coming weeks. Uncertainty regarding the new environmental laws and the cost of diesel (impacting sheep feed sourced from NSW) are two issues which will impact on producer decision making. The Queensland Committee’s fourth forecast of shorn wool production for 2025/26 is 8.50 Mkg greasy, down 7.9% on 2024/25.

2026/27 season. AWEX auction offerings from Queensland are expected to be down in the first few weeks, due to wool brought forward and sold in the last quarter of 2025/26. The Queensland Committee’s first forecast of shorn wool production for 2026/27 is 9.00 Mkg greasy, up 5.9% on 2025/26.

Appendix

Table A1: Comparison of shorn wool production in 2024/25 against the 2023/24 season and the fourth forecast for 2025/26 against the 2024/25 season. At their September 2022 meeting, the AWPFC National Committee resolved to include a clean estimate of shorn wool production based on the yield (%, Schlumberger dry top and noil yield) from the AWTA key test data for each complete season.

Note: Totals may not add due to rounding

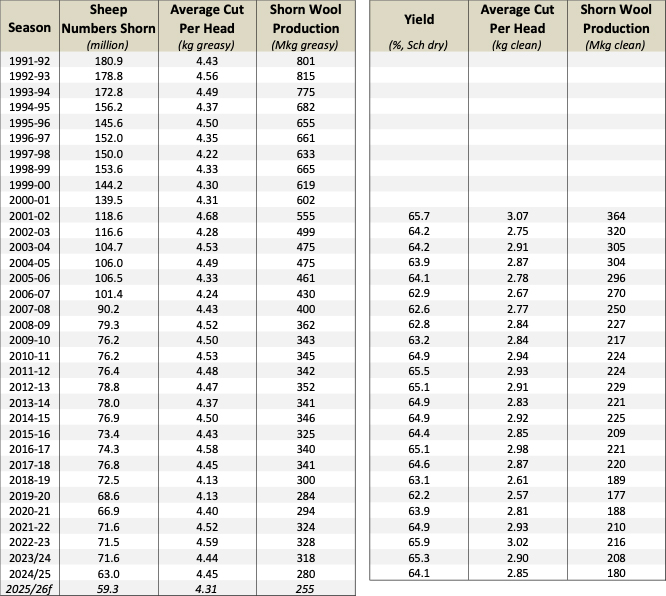

Historical Australian Production Figures

The tables below provide historical sheep shorn numbers, wool production, fleece weight and micron share statistics since 1991/92 for background information.

Table A2: Australian wool production statistics since 1991/92. At their September 2022 meeting, the AWPFC National Committee resolved to include a clean estimate of shorn wool production for each full season based on the yield (%, Schlumberger dry top and noil yield) from the AWTA key test data for that season.

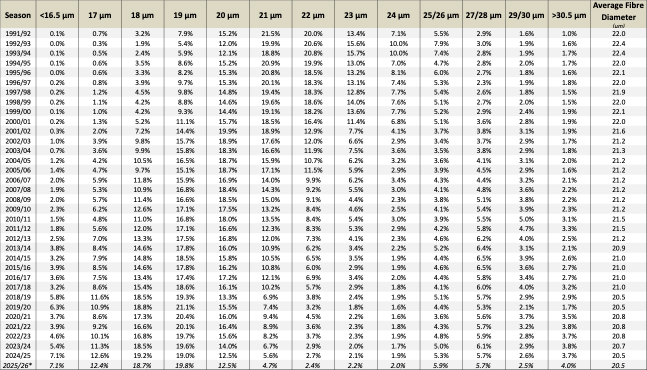

Table A3: Australian micron profile of AWTA wool test volume statistics since 1991/92 (% share and average micron)

2025/26* represents July to March

Explanation of revised AWPFC data series

At the December 2005 meeting, the National Committee made the decision to collate and review the key variables (shorn wool production, cut per head, number of sheep shorn) used in the committee from the available industry sources and to create a consistent historical data series at both a state and national level. This was required as some differences existed between industry accepted figures and the AWPFC data series and to ensure a consistent methodology over time. This process resulted in changes to the parameters ‘average cut per head’ and the ‘number of sheep shorn’ for some seasons at both a state and national level.

Modus operandi for the Australian Wool Production Forecasting Committee

The Australian Wool Production Forecasting Committee draws together a range of objective data and qualitative information to produce consensus-based, authoritative forecasts four times a year for Australian wool production.

The Committee has a two-level structure, with a National Committee considering information and advice from state committees. It is funded by Australian Wool Innovation Limited, which also provides a representative in the role of the Chairman of the National Committee.

The National and state committees comprise wool producers, wool brokers, exporters, processors, private treaty merchants, AWEX, AWTA, ABARES, ABS, MLA, state departments of Agriculture, sheep pregnancy scanners and AWI.

The Committee releases its forecasts in the forms of a press release and a report providing the detailed forecasts, historical data and commentary on the key drivers of the forecasts.